Being the pioneer of the Industrial Revolution made Britain the workshop of the world for much of the nineteenth century. That underpinned “the empire on which the sun never set” as British capital moved around the globe to lay down railways, dig mines and sow plantations. The colonies were defended by British arms. Their products were transported in British ships.

Empire had its downside, however. The economic interests most committed to it – primarily the City of London, the banks and finance houses that channelled capital for investment abroad and distributed the resulting dividends at home – became significantly counter-productive to British manufacturing. In every year over the century between the 1880s and 1980s, with the exception of the two World War years, Britain was a net exporter of investment capital abroad. No wonder its manufacturing industry declined over that time.

The UK’s economic history, of which Brexit is the latest episode, illustrates vividly the importance for a country of having a competitive currency exchange rate. It shows also how different ruling-class interests push divergent currency policies. If you are a City financier in the business of exporting capital you will want a strong national currency, for the stronger that is, the more foreign currency you will be able to get for it with which to invest abroad. However, if you are an industrialist trying to sell manufactured goods in foreign markets, you will want a weak and competitive currency, since that incentivises people abroad to buy your goods, while simultaneously discouraging competing imports.

Since the 1880s High Finance rather than Industrial Capital has dominated British economic policy. Throughout the nineteenth century the City of London was wedded to the gold standard. Government economic policy was similarly wedded. The City was behind the ruinous policy of going back on the Gold Standard after World War I at the same rate as in 1914. After World War II the City strenuously opposed various necessary devaluations of sterling. When these did happen its influence ensured they were never radical enough. The City lobbied to stay in the European Monetary System (EMS) which preceded the euro. When the high interest rates that were needed to keep Britain in the EMS threatened ruin for British industry and the UK left the EMS in 1993 – a step that boosted exports and economic growth – the City lobbied fiercely to join the euro. Luckily for the UK economy Labour’s Gordon Brown and the Treasury resisted City pressure. The Brexit referendum result was a bad blow to the City.

Britain’s foreign investments gave it global interests to defend. Germany and Japan were lucky to lose their empires following defeat in World War II. For decades after 1945 Britain spent 6% or more of its GDP each year on ‘defence’, much of it abroad, which was a drain on its balance of payments. German military spending averaged 2% a year. Japan’s was zero. Germany concentrated on domestic investment, using up-to-date technology. This made modern Germany a world leader in the export of high-quality manufactures, while Britain continued to export capital.

In the 1950s and 1960s Germany went straight from steam-driven trains to electric ones, while Britain wasted a generation on diesel locomotives. When Britain struck North Sea oil in the 1970s that strengthened the pound sterling, which in turn contributed to oil exports displacing its manufactures. Thus oil, a depleting resource, encouraged Britain’s long-term de-industrialisation. Norway was more sensible. The Norwegians sequestered their oil revenues in a special fund with which to buy foreign assets and encourage long-term investment. This prevented a strong currency exchange-rate which would have eroded their manufacturing base as happened in Britain. In 1972 one third of the UK’s GDP came from manufacturing. Today it is less than 10%, compared to 20% in Germany and Japan respectively.

A basic principle of economics is that raising productivity or output per head is fundamental to achieving higher living standards. This means producing more with less labour by giving workers better tools, machinery and technology; by raising workers’ skill-levels to make them better at using such instruments; or by giving them more effective energy resources. Investment in light manufacturing and in the high-technology-oriented side of the service sector is critical for this. That is because while investments in roads, schools, hospitals and housing, or in office blocks and restaurants, are hugely important in social terms, these lack the capacity to add value to the economy as a whole at a rate much faster than the rate of interest needed to finance them. Only investment in light manufacturing and high-tech services can give the longed-for big jumps in productivity.

Throughout the West today there is a decline in productivity and an accompanying low growth in living standards because of the dominance of High Finance over manufacturing and the resulting fall in investments in the productivity-enhancing areas of industry and skilled services.

Britain is an extreme example of this. It is a high-employment but low-productivity economy. As regards employment some 75% of British people aged 15-64 are in work, compared with 74% in Germany, 73% in Japan, 69% in the USA, 64% in France, 60% in Ireland and 57% in Italy. The UK unemployment rate is now only 4%. When it comes to productivity or output per person per hour worked however, the UK is only 76% of the US level, 78% of the French and 79% of Germany’s.

The UK’s poor productivity is due to its low rate of investment, particularly in manufacturing, and a low rate of savings to finance those investments. At present the UK invests less than 13% of its GDP in physical assets. The world average is some 25%. In China it is nearly 50%, one-third of that in productivity-enhancing projects.

John Mills is a British businessman whose firm exports to some 80 countries. He is also an economist with ten books to his credit. He is a member of the British Labour Party, a joint chairman of Business for Britain and the founder of Labour Leave which campaigned for Brexit in last year’s UK referendum. In my opinion his recent book, ‘Britain’s Achilles Heel: our uncompetitive pound’ (Civitas 2017), which builds on a lifetime’s economic work, merits his getting a Nobel economics prize for the way in which it shows how the competitive currency exchange rate that allows domestic economies to flourish is critical for the welfare of the mass of people everywhere. High Finance and banking interests take a different view. They prefer strong currencies. Most academic economists, with their susceptibility to intellectual fashion, have tended to go along with them.

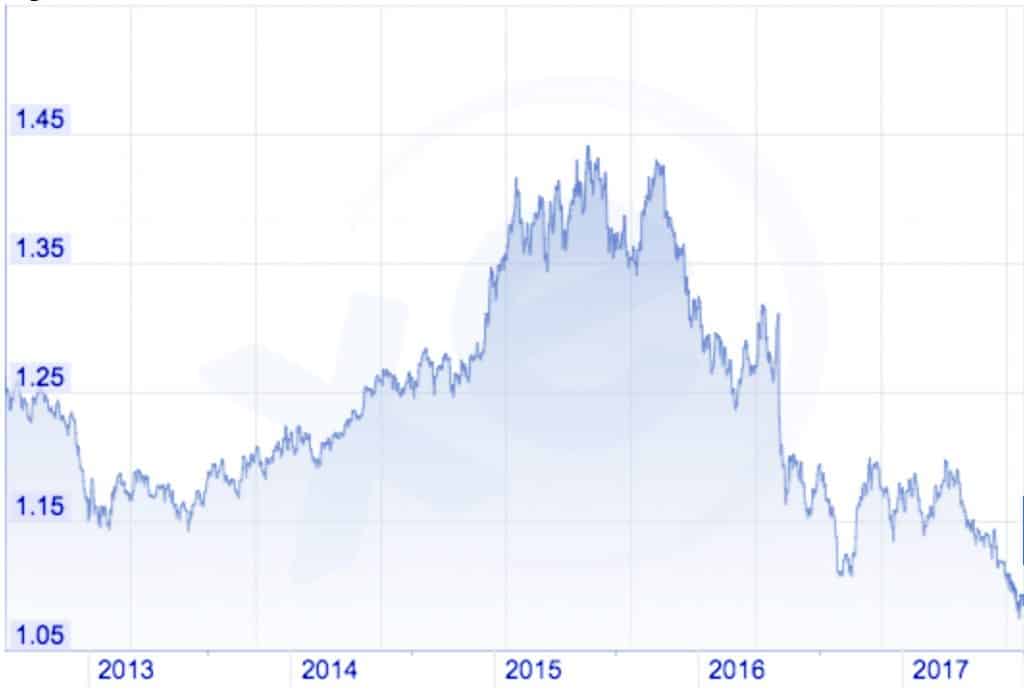

Mills’ book is very relevant to Ireland. We experienced the benefits of a highly competitive exchange rate when we effectively floated the Irish pound following the devaluation of 1993 when we were forced to leave the EMS. This underpinned our ‘Celtic Tiger’ rate of 8% average annual economic growth between 1993 and 1999. Then Ireland’s Great and Good, impelled by the usual euro-zealotry, abolished the national currency in order to adopt the euro. We are now stuck with an overvalued euro, which is hitting our exports to the US and UK, our most important single-country markets, while the pound sterling falls as it is likely to continue to do while the UK negotiates Brexit.

If the UK is to make a success of Brexit, from its point of view it will have to change radically its traditional economic policies. Foremost it must put the City of London, with its cult of a strong currency, in its place and adopt policies instead to counter the UK’s de-industrialisation. The most important such policy is for the UK to get right the cost base for internationally traded goods and services. As Mills’ book shows, this requires above all a radically weaker sterling exchange rate.

Throughout the West today there is a decline in productivity and an accompanying low growth in living standards because of the dominance of High Finance over manufacturing and the resulting fall in investments in the productivity-enhancing areas of industry and skilled services.

Supportive policies will then be needed to increase savings and encourage productivity raising investments. After decades when it was out of fashion Theresa May’s government is now talking once more of “industrial policy”. If this is to have substance it means bank credit and tax policies to encourage industrial investment and R & D, and a shift in education policy from concentration on expanding access to universities to emphasising vocational training, encouraging apprenticeships and adult education generally. This seems a tall order against the background of Britain’s economic history. But it is what the situation requires if Brexit is really to be a positive turning-point for the UK.

Anthony Coughlan is Associate Professor Emeritus in Social Policy, Trinity College Dublin

![]()